The United States is home to some of the world’s most advanced medical technology—and arguably the world’s most expensive bills. For international visitors, a sudden illness or injury in the USA is not just a health crisis; it is a financial catastrophe waiting to happen.

If you are planning a trip to the US, or if you are a US resident inviting family members from abroad, understanding Travel Medical Insurance is critical. Unlike comprehensive “trip protection” policies that focus on lost luggage and flight cancellations, Travel Medical Insurance is a specialized product designed to pay for doctors, hospitals, and ambulances.

But here is the million-dollar question: If you buy a policy, what does it actually cover?

This guide dissects the fine print of Travel Medical Insurance for the USA. We will reveal the standard inclusions, the surprising exclusions, and the “grey areas” like pre-existing conditions and pregnancy that trip up thousands of travelers every year.

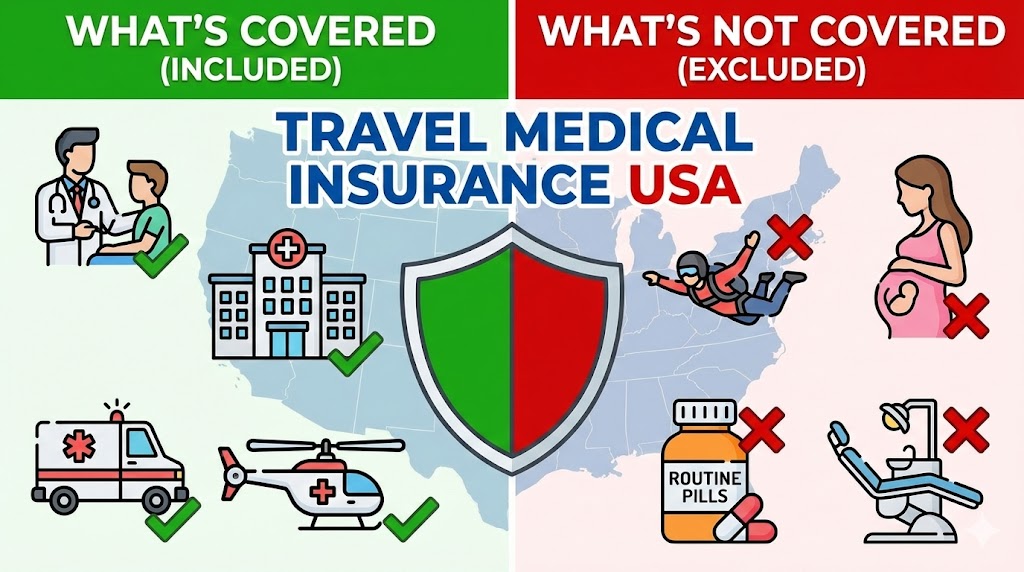

The “Big Three” Inclusions: What is Always Covered?

When you purchase a reputable comprehensive visitor insurance plan (from providers like Seven Corners, IMG, or WorldTrips), you are primarily paying for three core protections. These are the pillars of your policy.

1. New & Unexpected Sickness or Injury

The fundamental rule of travel insurance is that it covers the unforeseen. If you are healthy today, fly to New York tomorrow, and break your leg or catch pneumonia, you are covered.

- Eligible Expenses:

- Hospital Room & Board: The daily cost of the hospital bed and nursing services (avg. $4,000/day in the US).

- Physician Fees: Bills from surgeons, anesthesiologists, and specialists.

- Diagnostics: X-rays, MRI scans, and blood tests ordered by a doctor to diagnose your new condition.

- Prescription Drugs: Medication prescribed after the injury/illness occurs (e.g., antibiotics, painkillers).

2. Emergency Medical Evacuation

This is the benefit that saves lives. If you are injured in a remote area (like a national park) or if the local hospital cannot treat your specific condition, “Evacuation” pays to transport you to the nearest adequate facility.

- Coverage Limit: Look for at least $100,000.

- Real-World Example: You suffer a stroke while visiting the Grand Canyon. A helicopter airlift to a trauma center in Las Vegas can cost $40,000. Your insurance pays this directly.

3. Repatriation of Remains

It is a morbid topic, but a necessary one. If a traveler passes away while in the USA, the cost to transport their body back to their home country is significant ($10,000–$15,000). This benefit covers the logistics and costs of returning the deceased to their family.

The “Grey Area”: Pre-Existing Conditions

This is the #1 reason for denied claims. A pre-existing condition is any medical issue you had before the policy started (e.g., diabetes, hypertension, heart disease).

What is NOT Covered? (Routine Maintenance)

Travel insurance is not health insurance. It will not pay for:

- Routine check-ups (e.g., “I want to see a US doctor to check my blood sugar”).

- Prescription refills (e.g., “I forgot my blood pressure pills”).

- Expected treatments (e.g., “I need dialysis every week”).

What IS Covered? (Acute Onset)

Top-tier plans (like Patriot America Plus or Atlas America) offer coverage for the Acute Onset of a Pre-Existing Condition.

- Definition: A sudden, unexpected recurrence of a pre-existing condition that requires immediate medical attention within 24 hours.

- Example: Your father has managed high blood pressure for 10 years. While in the USA, he suffers a sudden, life-threatening heart attack. This is an “Acute Onset” and is typically covered.

- The Catch: This coverage usually expires or reduces significantly once the traveler turns 70 or 80 years old.

Common Exclusions: What is Never Covered?

Travelers are often shocked when their claims are rejected for these reasons. Knowing these exclusions in advance can save you thousands.

1. Routine & Preventative Care

US healthcare is expensive, so tourists sometimes try to get “health check-ups” while visiting. Insurance will reject 100% of these claims.

- Excluded: Physical exams, vaccinations, teeth cleaning, eye exams, and pap smears.

2. Maternity & Childbirth

Standard travel medical insurance is not maternity insurance.

- Excluded: Prenatal check-ups, ultrasounds, and normal delivery. If you travel to the USA to give birth (birth tourism), you will pay the $15,000+ hospital bill yourself.

- Exception: Some plans cover Complications of Pregnancy (e.g., threatened miscarriage, pre-eclampsia) during the first 26 weeks of gestation. Once you enter the third trimester, almost all coverage ceases.

3. High-Risk Adventure Sports

Did you come to the USA to ski in Colorado or surf in Hawaii? Check your policy.

- Excluded: Skydiving, bungee jumping, backcountry skiing, and sometimes even organized contact sports.

- Solution: Buy a “Sports Rider” or “Adventure Sports” add-on. Plans like World Nomads or Atlas America are famous for including many of these activities automatically.

4. Mental Health Disorders

Most standard visitor insurance plans exclude treatment for mental and nervous disorders, including depression, anxiety, and substance abuse rehabilitation, unless you purchase a specialized student plan.

Dental & Vision: The “Pain” Clause

Do not expect your travel insurance to buy you a new pair of glasses or a root canal.

- Dental Coverage: Is usually limited to “Acute Onset of Pain” or “Injury to Sound Natural Teeth.”

- Scenario A: You wake up with a toothache. The policy might pay $100 to $300 for palliative care (pain relief) only.

- Scenario B: You fall and knock out a tooth. The policy covers the repair up to the policy maximum (or a specific dental limit) because it is an accident.

- Vision Coverage: Almost non-existent. If you break your glasses, you buy the replacement.

COVID-19 Coverage in 2026

The pandemic changed the insurance landscape. Today, COVID-19 is treated like any other illness by most reputable insurers.

- Medical Bills: If you catch COVID-19 in the USA and need hospitalization, it is covered up to your policy limit.

- Testing: Only covered if ordered by a physician because you are symptomatic. Voluntary tests for travel clearance are not covered.

- Quarantine: This is distinct from medical coverage. If you test positive and have to stay in a hotel for 5 days but do not need a hospital, Medical Insurance pays $0. You need a policy with a specific “Trip Delay” benefit to get reimbursed for the hotel and meals.

FAQ: Travel Medical Insurance Coverage

1. Does travel insurance cover my prescription medication?

Only if the medication is prescribed during your trip for a new injury or sickness. It will not pay to refill the maintenance medications (like cholesterol pills) you take every day at home. Bring enough supply for your entire trip!

2. Can I go to any doctor, or do I need a “Network” doctor?

Most plans allow you to go to any doctor, but you save money by staying In-Network.

- In-Network (PPO): The doctor bills the insurance directly (Cashless). You pay only your deductible.

- Out-of-Network: You pay the full bill upfront and file a claim for reimbursement later. This is risky because the insurance might say the doctor charged “unreasonable” rates and only pay a portion.

3. What happens if I am intoxicated?

If you are injured while under the influence of alcohol or drugs (above the legal limit), your claim will likely be denied. If you get drunk and fall down a flight of stairs, the insurance company can legally refuse to pay the ER bill.

4. Is “Urgent Care” covered?

Yes, and it is highly recommended! Urgent Care clinics are much cheaper than Emergency Rooms. Many plans (like Trawick Safe Travels) even have a small fixed copay (e.g., $30) for Urgent Care visits, making it the most affordable way to see a doctor for minor ailments like the flu or a sprained ankle.

Conclusion

Travel Medical Insurance for the USA is a safety net, not a blank check. It is designed to save you from bankruptcy due to accidents and emergencies, not to maintain your general health.

The Golden Rules of Coverage:

- It covers the Unexpected: New accidents, new illnesses, and emergency evacuations.

- It excludes the Routine: Check-ups, vaccines, and maintenance meds.

- It requires caution: Pre-existing conditions are only covered if they are “Acute Onset,” and high-risk sports require extra riders.

Before you fly, read the “Exclusions” section of your policy document (usually found on page 5 or 6). Knowing what is not covered is the best way to ensure that when you do need help, you are fully protected.

Get a Quote Today:

Don’t guess. Visit a comparison site like Insubuy or VisitorsCoverage to see the exact coverage details for plans like Patriot America and Atlas America side-by-side.